A Crazy Week in the Credit Markets – The Fed has Lost Control!

How an over-levered company should approach refinancing

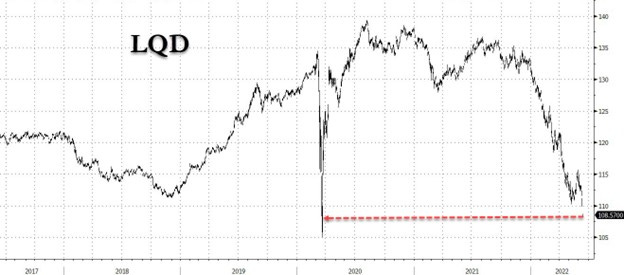

$LQD ETF just crashed – what does that mean?

This can be a dry subject but we’ll try to make it interesting for you. We’ve got lots of graphs in this article so hopefully you are a data nerd like us. Let’s start out by looking at iShares Investment Grade Corporate Bond ETF ($LQD)…

Corporate bonds are falling off a cliff as investors realize that a lot of companies won’t be able to pay off their debt at higher interest rates. After years of 0% interest, a lot of companies took on too much cheap debt, often tied to LIBOR or other floating rate instruments. With interest rates rising, companies will need to refinance at much higher rates than previous rounds.

Baa Corporate rates have more than doubled since Dec 21; every $50M in debt equalling another $1.2M in interest expenses with companies needing to refinance. It’s alarming stats like these that is causing the $LQD to drop to levels at or below the 2020 pandemic.

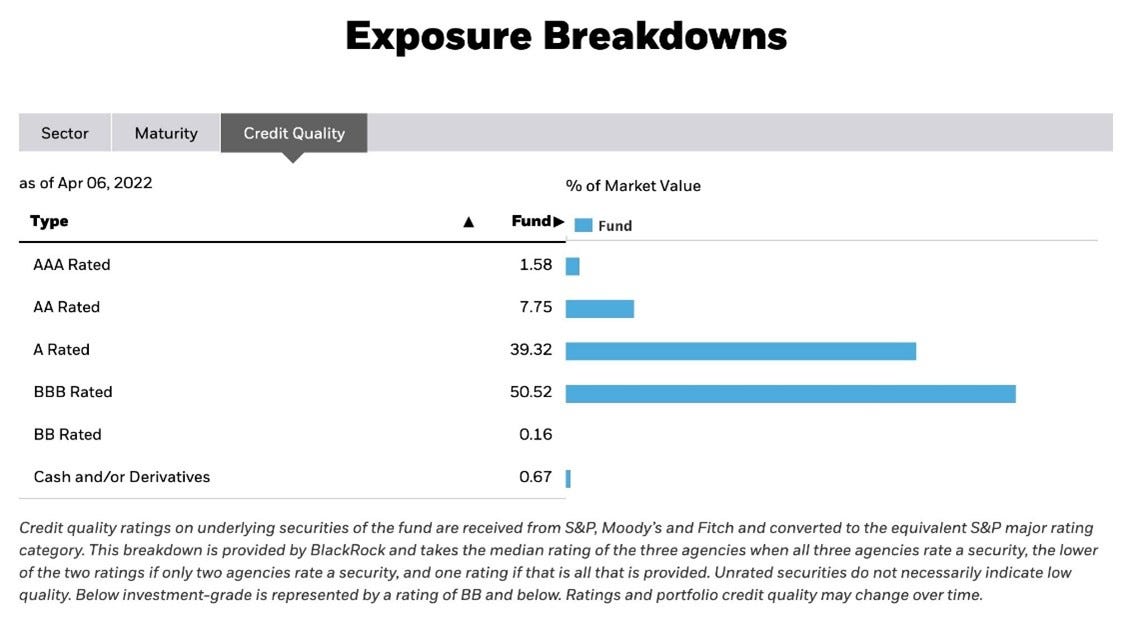

A deeper look into $LQD shows that it’s comprised of lower quality rated investment grade bonds. If the BBB rated funds get downgraded (high risk of this happening) then they are no longer investment grade, meaning many pension and mutual funds will need to sell. This would create another big shock to yield rates, making refinancing even more expensive.

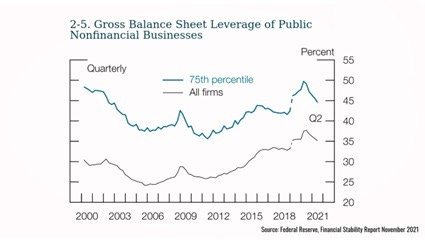

Corporations have levered their balance sheets up to 45% of total capitalization versus 25% heading into the 2008 financial crash. The reaction in the equity markets post- 2008 crash was to simply borrow more for additional liquidity. However, companies have already pulled that lever, with many in the 75th percentile (most levered) considered at extreme levels of debt. These companies already are tapped out with no more ability to raise more debt.

We are looking at a high risk of a “Downgrade Cascade” – I’ll explain. A BBB rated company’s EBITDA falls due to high inflation thus having a less income to service it’s debt. Therefore, the debt is downgraded causing investment grade credit funds to sell off those debt instruments. The price of debt drops creating higher servicing costs in the future. Markets will need to compensate for the credit spread risk, pushing rates even higher. The probability of default increases, making it difficult to raise new debt and down the spiral we go. Here is a chart laying out the cascade effect in a clearer manner.

Downgrade Cascade Chart

What is the Fed’s role in this mess?

During the pandemic the Fed reacted by “printing” trillions in new currency, making cheap debt very easy to raise. As a result, the private debt markets were awash in capital chasing a smaller pool of high-quality deals. Therefore, they started to look for yield returns in the leveraged loan space. These are loans issued to companies with weak balance sheets at leverage or interest coverage ratios far in excess of industry norms. Rapid growth was seen in the leverage loan space, often with credit agreements that are covenant lite.

Smart money, like Oaktree Capital Management and JP Morgan, have been working hard in anticipation of these market conditions, recently announcing new special situation funds to capitalize on credit constraint companies. Both funds surpassed $2B in seed funding to target North America and Europe.

The covenant lite aspect of many high leverage loans will be beneficial to these new funds as it will allow them to acquire and restructure them more cheaply than covenant heavy agreements. We expect Oaktree and JP Morgan to attempt to gain equity control or at least move up the capital stack with each investment. However, at the very least, being covenant lite will allow them to benefit from the increasing credit spreads as BBB’s intrinsic value falls less then the price would suggest as they become casualties of the pension and mutual fund downgrade cascade effect.

The Federal Reserve has now reversed course due to spiking inflations (printing trillions of dollars will do that) and have entered a Quantitative Tightening phase by shrinking its balance sheet, in order to raise rates. This started on June 1st so the ripples are only now being felt by borrowers who are starting to refinance. We expect Bank of Canada to follow their US counterparts lead in order to keep the CDN/USD foreign exchange rate in an acceptable range so don’t expect anymore cheap debt in Canada either.

So far we have…

1. Corporate bond markets crashing —> creating increasing refinance rates

2. Many companies who are already over-levered —> high valuation sensitivity to refinance rates

3. An expected oversell off in BBB bonds —> making it even more difficult (vs. investment grade) for high levered companies to refinance

4. Smart money looking for distressed companies à high risk of activism in capital stacks

5. Federal Reserve has begun quantitative tightening à reduction in amount of remaining cheap debt

Ok so lots of bad news. Is there anything companies who fall into the BBB or lower category to do?

We think the traditional methods of refinancing, especially for BBB or lower companies are becoming too expensive. Therefore, these companies need to get creative and understand where to look in the credit markets that would make a refinancing financial possible.

The good news is that dry powder is still plentiful in the market with over $400B in private debt still sitting on the sidelines looking for yield. With rates rising through, companies will need to structure deals in different ways to attract those funds and do it quickly before the activist investors like Oaktree come knocking.

Responding to this new environment, many funds are responding to PIK loan positions. These are hybrid of debt and equity, being one of the rescue capital financial products that are growing in popularity. Especially in the middle market, where senior lenders are much more nervous, PIK loans offer new dollars to BBB or lower companies that help manage cash flows until operational issues like inflation and supply chain challenges are figured out. PIK loans, defer cash interest payments, paying out the creditor with more securities, thus preserving precious cash.

Funds with dry powder who have been crowded out by funds with cheaper money, raised during the pandemic, can find yield by sitting lower in the capital stack. If they feel the company with less of a cash burden can turnaround after solving for operational issues will earn equity like returns or structure the PIK loans so that cash interest is resumed once EBITDA is above water.

Creative structuring in PIK loans can help to find a win-win scenario for both company and private debt fund with the loan sitting in part common, preferred or convertible along with a cash portion. There are many different ways for companies to approach these types of lenders rather than just accepting a higher interest rate, they are unlikely to be able to service.

Working with an investment bank like Clariti can help find these pockets of dry powder and advise on the PIK structure that will help get to a post turnaround situation. This will help ownership preserve equity values and allow for future growth.