Don't be Afraid of SAFE Notes

A simpler type of convertible notes to help finance a particular type of turnaround

At the time of writing this article, we are analyzing the acquisition of a manufacturing company with a unique set of circumstances. Here is what I tweeted out a few days before…

This is a classic balance sheet turnaround situation but I’d call it unique because even though the balance sheet is a mess, the operations are exceptionally well run. Essentially what happened here was pre-COVID, a new owner paid 7x SDE a the company using 90% SBA debt, with the expectation of quick future growth. During COVID, he found out customer relationships weren’t as stick as he initially modelling, in fact, many would have left him anyways. His revenue declined and was hard pressed to carry the P&I on the acquisition loan. To his credit, he runs a tight ship and was able to develop proprietary IT to leapfrog ahead of his competitors with an easy to order cloud bases system (many of his competitors were still in the fax machine age).

With a balance sheet this under water, you are unlikely to find another debt provider to take on operating losses with a mostly uncollateralized loan (the owner doesn’t have a personal balance sheet to support the gap). Even my friends in the “stretch capital world” would have a hard time getting their arms wrapped around this deal so what options could this company look at?

We’ll the first thing that would come to mind is either chapter 11 or find an equity partner. However, those 2 options are very expensive or could damage the companies long term reputation. We don’t see them as an option at this stage of the turnaround.

I wasn’t not immediately turned away from the deal because I see a smart owner who has really built some excellent systems (ordering, inventory management, new sales processes). Given the tight ship he runs combined with a huge industry, national reach and much improved sales processes, I think this could be a diamond in the rough that needs a better balance sheet to grow. Enter SAFE notes…

Traditionally, SAFE notes or Simple Agreement for Future Equity, has traditionally been used by VC’s for the startup world but I’m arguing here that this tool could be used for the turnaround world under a particular set of circumstances. SAFE Notes use a simple 5 page contract structure to raise funds without interest rates or maturity dates. Only valuation caps are negotiable. It’s similar to an option or warrant to buy shares of the company in a future round and is NOT debt which could allow a bank to feel comfortable enough to not cash in all their chips. In this situation, we’d be betting on the owner to grow revenue - since the operations are tight, this could start immediately and would only need to raise $4M (the gap) vs. the entire $6M which is the current value of the bank secured loan.

ADVANTAGES OF SAFE NOTES

Simplicity

Easy to negotiate

Distressed company flexibility (no pre-determined maturity date)

Conversion to Equity (can happen after turnaround is complete & future equity rounds are raised)

DISADVANTAGES OF SAFE NOTES

Not an official debt instrument (thus less security)

Fair valuation expense (trigger the need for a fair valuation, which is costly & diverts funds from the turnaround)

Likely no dividends like a common shareholder (this is fine if your goal is to gain equity)

Dilution (future SAFE Note rounds dilute the current investors)

SOME GENERAL SAFE NOTE TERMS

Valuation Cap - sets highest price that can be used for conversion (vs. convertible debt which includes a discount)

Early Payback Exit - notes can be paid out to the buyer if an acquisition or change of control should occur prior to the regularly expected conversion

Conversion - can convert with any dollar amount during a preferred cycle

Term Date - there is no maturity so you could be waiting a long time to maturity even if the company is profitable

Interest Rate - there is no interest rate, unlike convertible notes

THINGS TO CONSIDER

Consider investing only with a cap on the SAFE Note (vs an uncapped note) and negotiate with a low cap amount - like we’d be trying to do with this investment

Don’t enter a SAFE note investment if there are many rounds with different limits on them

SAFE Notes should be considered a bridge form of financing due to the dilution rates they pose on earlier rounds, so we’d need to ensure this company can execute on the turnaround and re-enter the debt world in the future (no more SAFE Note rounds) so we can profitability exit this unique investment.

With respect to valuation - with no interest rates or set maturity dates, your only leaver as an investor is to negotiate a low valuation cap. Your goal is not to miss out on the appreciation of the company assets between the investment and raising of the next round, allowing you to convert the SAFE Notes.

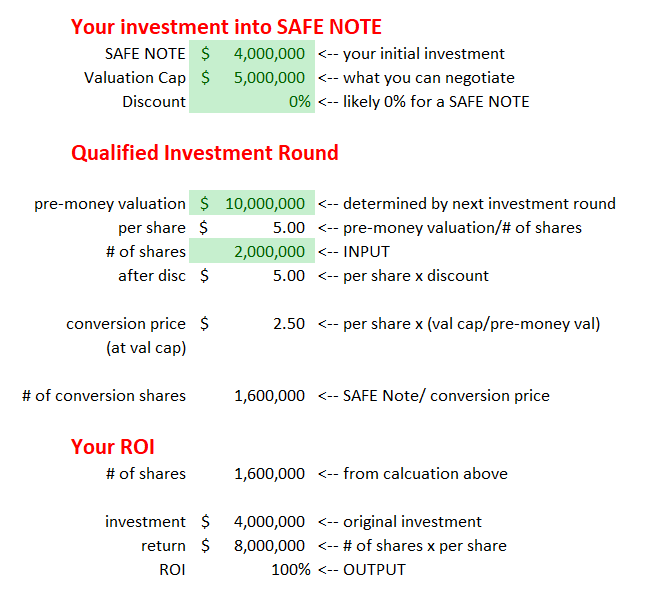

EXAMPLE OF A VALUATION CAP

Valuations caps are not company valuations (like DCF or P/E). Leave that exercise to the common rounds. In this example, I’m assuming that the bank would continue to fund if fully collateralized ($2M) so a $4M SAFE Note is needed. If we believe that in 2-3 years, that the improved processes put in place by the owner can yield a profit of $2M, then a $10M pre-money valuation before the next round is reasonable. Therefore, the valuation cap calculator shows me that a 100% ROI on the investment is achievable. At the next round, we’d convert a SAFE Note, worth $2.50 into a $5.00 per share valuation. I’m assuming in the SAFE Note contract that the $10M next round is qualified & allows me to proceed with the conversion to equity.

The key questions you’ll need to ask yourself when making a SAFE Note investment is..

What would the next round look like (no more SAFE Notes to avoid dilution)

Will the turnaround plan yield a pre-money valuation in excess of a per share price less a discount%?

What are the chances of the turnaround plan occurring in a reasonable period?

This should give you an introduction to SAFE Notes. In the future, I’ll talk more of the comparisons to convertibles as they do share many traits but given the nature of this companies balance sheet and a nervous senior creditor, it could be an option if you believe in the turnaround’s ability to succeed.

Michael, Thanks for the analysis on this deal using SAFE Notes. I have a rock quarry that I'd like to visit with you about.

JD