The Asymmetric Risk/ Return Threshold & It's Impact on Distressed Investing

Think of assessing each opportunity like it were an stock options contract

The concept of risk and return is often a well covered topic and much talked about in financial literature. What is overlooked, however, is understanding what is an acceptable threshold between your risk (downside) and return (upside) especially when evaluating a distressed investment.

I see the concept of pricing of stock option contracts as having similar risk/reward thresholds as what I do for a living - fixing broken companies then flipping them for a profit.

A stock option is the right to buy a number of shares in the future at a pre-set price, known as a “strike” price. In return for the right to buy $GE, currently trading at $13.44 per share for a strike price of $13.15 in 2 weeks, an investor will have to pay a certain amount for that right. The amount paid is the value of the options contract and that value is determined by the Black- Scholes model.

Not to get too technical or put you to sleep, the valuation of the options contract is based on several factors including using the normal distribution of expected (implied) volatility of that stock.

The normal distribution, which is a statistics term, basically says there is a 68% chance that a stock will trade within 1 standard deviation of it’s current price. The 1 standard deviation calculation is based on prior price volatility. Bitcoin, which is highly volatile will have a wider variance, say 20% implied volatility vs. $IBM, a slow growth blue chip company, with it’s 5% implied volatility.

However, smart investors know that stocks don’t always move that way - they can be prone to large price spikes, say around earnings release season or if Elon Musk tweets about it frequently. An investment that includes an excessive number of large positive price spikes will have what is called “positive skewness”.

In this case, if the Black- Scholes has valued the options contract using normal distribution but the stock tends to act with positive skewness, then they can shrewdly arbitrage the opportunity for a profit.

Positive Skewness = probability of an unexpected upwards spike in the stock (return) is greater than an unexpected downwards movement (risk). Combine this equation with the price paid for the options contract, it’ll give you a better price of the investments risk/ return profile.

Alright, so this is interesting but what does it have to do with distressed investing? We are taking that same concepts of…

Probability (large upwards spike) > Probability (downwards spike)

Known & quantifiable amount of risk, as represented by the cost of an options contract

Then incorporating them into our decision making thesis for a distressed investment. Let’s stick with stocks options as an example (assume implied volatility = 15% for a $40/share stock)…

Return - 73% probability of greater than implied volatility

Risk - 27% probability of less than implied volatility

Option Price - $2.00

Therefore, the probability adjusted return/ risk is 1.38 (or 2.76/2). Since this number is greater than 1.00, the risk adjusted return for a stock with positive skewness is greater than the risk of buying the contract.

Let’s leave stock options and move this example to investing in a distressed company, however, let’s take a quick refresher on what risk represents.

I think of risk as 2 components —> what I have to pay for the company/ assets + can I turn the company around to generate a rate of return.

The first component of risk is a little more obvious. It’s the cash investment required to acquire the assets or shares of a company. Where this gets a little more complicated than stock options is the potential off-balance sheet liabilities such as law suits that you may haven’t uncovered in due diligence so make sure you have considered that risk during due diligence.

The second component, realizing the upside, is where a bit of the art of the turnaround comes into play. Remember, you are asking yourself; “this an (significantly) underperforming asset, what am I going to do differently in the future to change that?” Once you are projecting into the future you are destined to have some forecasting error.

Using Probability Scenarios - calculating Risk Adjusted Returns

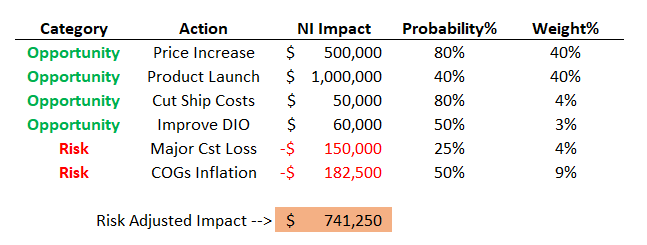

Similar to the arbitrage of a stock options contract, we need to find turnaround situations with positive skew of probability distributions. If those risk adjusted returns outweigh our known risk (cash investment assuming no liability surprises) by an x times factor, then it’s a calculated risk I’d want to take. The positive skew is derived from an expectation that the # of upside opportunities is approximately 73% of all potential actions. For example, let’s use a widget manufacturer with the following TTM P&L..

Our goal here is to acquire this money losing widget manufacturer and turn it into a cash machine. Let’s assume we paid $1.5M for this company and there are no post- acquisition surprises.

After an initial assessment of the business, pre-acquisition, we have uncovered the following list of hypothetical turnaround actions to improve performance…

Note - I’ll spend more time on how to calculate probabilities in another article using a process called Monte Carlo Simulation & how some actions need to be done in sequence to achieve the expected probability. For instance, I can’t get a shipping cost cut without more volume from a new product launch, as the extra volume allows me to ship full truck load vs less than full truck load. Therefore, the probability will start to follow a “tree-like” pattern - one action will significantly impact another. However, I’ll keep it simple for this session.

I’ve laid out 4 opportunities and 2 risks. By offsetting those Net Income (NI) impacts against the probability % of how likely they are to come to fruition, we have a total risk adjusted impact of $741K.

Another calculation I made was “Weight %” which is how I’m measuring if this is positively or negatively skewed turnaround. By summing the 4 opportunities and the 2 risks I get…

So I really this skew - I get a much higher chance of a positive impact than a negative one based on my assessment. The probability weights from my pre-acquisition assessment tips the scales in my favor enough to make me feel confidence this is a good risk.

Measuring the Bet - Does the level of returns for a turnaround justify the risk?

Let’s revisit the P&L assuming all the turnaround actions actually happened…

We turned this business from a money loser to a nice profitable little company with some key initiatives that prior ownership was unable or unwilling to execute on.

Our cost to acquire the business was $1.5M and after baking in the turnaround tactics would support a valuation of $9M or about x12 EBITDA. Therefore our downside (or options contract) was $1.5M and our upside was $9M, however the key question to ask is was this “asymmetric enough to justify the risk?”

My rule of thumb is I need a x5 rate of return to think about doing the turnaround. This hypothetical situation yields me a x6 return after considering all the upside/downside movements that could happen. This is an investment I would make!

I hope this article gives you a little more flavor on how we look at risk adjusted returns when thinking about a distressed investment. Because we know ahead of time that each opportunity has a level of risk built in, we need to ensure that not only is the overall opportunity worth it but that we have enough upward opportunities that outweigh the potential downside risks. I want to look at each business turnaround like a stock option contract help manage risk and ensure I’m betting on the situations that will give me the best chances of success.